Intel Stock Gets Rare Double Upgrade From Bank of America: Here's Why

Intel Corp. (NASDAQ:INTC) shares jumped over 7% Thursday after Bank of America Corp. handed the chipmaker a rare double upgrade, lifting its rating two notches — from ‘Underperform’ straight to ‘Buy.’

Analyst Vivek Arya also raised the firm’s price objective on Intel from $96 to $135, implying roughly 26% upside from Wednesday’s close.

A double-upgrade skips the usual Neutral way station and jumps straight from sell to buy. They are rare.

Banks reserve them for moments when the thesis they were betting against breaks.

Arya now sees “higher confidence in INTC's opportunity to help address industry constraints in leading edge wafers/packaging, plus supply into a much larger agentic CPU TAM."

Bank of America now models Intel’s earnings power at more than $6 per share by 2030, up sharply from a prior $3-to-$4 range.

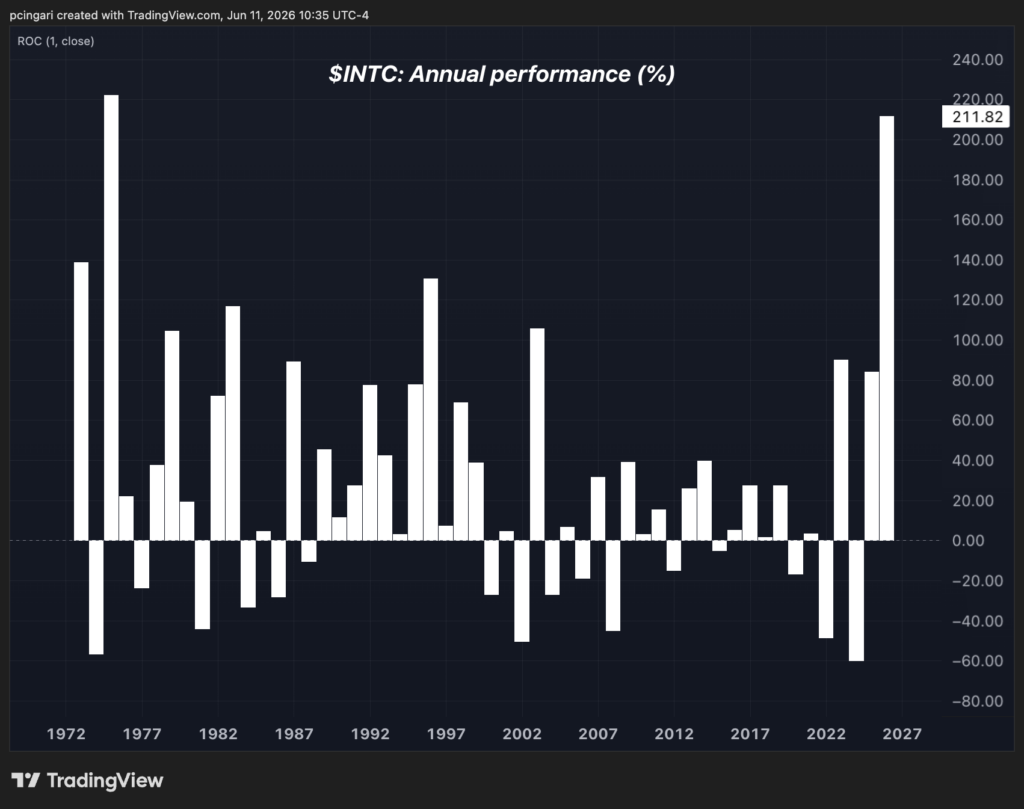

Intel has been one of 2026’s best stocks, surging roughly 210% year-to-date and putting it on pace for its best annual showing since 1975.

Why It Matters: CPUs And Foundry

On the product side, Bank of America expects Intel’s central processing unit, or CPU, sales to top $40 billion by 2030, or about 25% of a $170 billion total addressable market.

Arya frames the CPU as a structural winner from the shift toward agentic AI, where the processor moves from feeding GPUs to orchestrating autonomous reasoning loops, memory state and tool use.

The firm pegs the combined AI compute/head-node and agentic-node CPU opportunity at roughly $140 billion within a $2.1 trillion data-center systems market by 2030.

Intel is also a foundry, meaning it manufactures chips for other companies.

Bank of America values a foundry opportunity above $45 billion by 2030 spanning potential work for Apple Inc., MediaTek and others, helped by a recent Cadence Design Systems Inc. tie-up on Intel’s 14A process node.

Intel Is Still Under-Owned

Bank of America also flagged Intel as deeply under-owned.

Despite a market cap above $540 billion — fifth-largest in the semiconductor and AI-infrastructure group — Intel sat in just 16% of S&P 500 fund portfolios as of May, the second-least-owned name in the cohort after SanDisk Corp. (NASDAQ:SNDK).

Arya drew a parallel to Advanced Micro Devices Inc. (NASDAQ:AMD), whose ownership climbed roughly 1,400 basis points year-over-year to 39% as the stock rose more than 300% — suggesting room for Intel’s investor base to broaden.

Yet, there are also cautionary signals. Arya cautioned that execution remains the swing factor.

Key risks include intensifying competition from Arm-based and custom CPUs, a potential moderation in AI capital spending that could weigh on CPU demand, and execution risk in design and manufacturing at Intel’s 18A and upcoming 14A nodes.

Power and cost constraints also feature. Still, with the server CPU market expanding about 40% and the chip’s role structurally widening, Arya expects a multi-year upgrade cycle ahead.

From a valuation perspective, Intel trades near 100 times this year’s expected earnings, among the richest multiples in the chip sector.

Image: Shutterstock