Exploring Aramark's Earnings Expectations

Aramark (NYSE:ARMK) will release its quarterly earnings report on Monday, 2025-11-17. Here's a brief overview for investors ahead of the announcement.

Analysts anticipate Aramark to report an earnings per share (EPS) of $0.65.

The announcement from Aramark is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

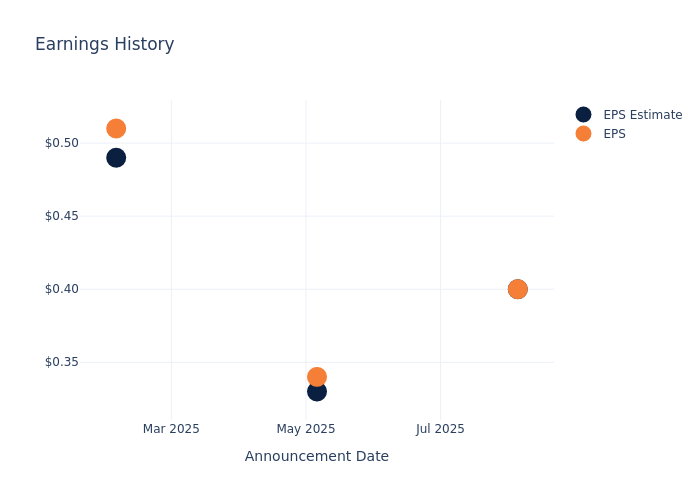

Overview of Past Earnings

In the previous earnings release, the company missed EPS by $0.00, leading to a 0.22% drop in the share price the following trading session.

Here's a look at Aramark's past performance and the resulting price change:

| Quarter | Q3 2025 | Q2 2025 | Q1 2025 | Q4 2024 |

|---|---|---|---|---|

| EPS Estimate | 0.4 | 0.33 | 0.49 | 0.53 |

| EPS Actual | 0.4 | 0.34 | 0.51 | 0.54 |

| Price Change % | 0.0 | 2.00 | 1.00 | -2.00 |

Stock Performance

Shares of Aramark were trading at $38.53 as of November 12. Over the last 52-week period, shares are up 3.44%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analyst Observations about Aramark

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Aramark.

Analysts have provided Aramark with 1 ratings, resulting in a consensus rating of Buy. The average one-year price target stands at $45.0, suggesting a potential 16.79% upside.

Analyzing Ratings Among Peers

This comparison focuses on the analyst ratings and average 1-year price targets of Texas Roadhouse, Dutch Bros and Cava Group, three major players in the industry, shedding light on their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for Texas Roadhouse, with an average 1-year price target of $187.08, suggesting a potential 385.54% upside.

- Analysts currently favor an Outperform trajectory for Dutch Bros, with an average 1-year price target of $75.33, suggesting a potential 95.51% upside.

- Analysts currently favor an Neutral trajectory for Cava Group, with an average 1-year price target of $70.44, suggesting a potential 82.82% upside.

Insights: Peer Analysis

The peer analysis summary outlines pivotal metrics for Texas Roadhouse, Dutch Bros and Cava Group, demonstrating their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Aramark | Buy | 5.72% | $370.11M | 2.35% |

| Texas Roadhouse | Neutral | 12.83% | $211.51M | 5.71% |

| Dutch Bros | Outperform | 25.24% | $106.78M | 2.71% |

| Cava Group | Neutral | 19.86% | $72.37M | 1.94% |

Key Takeaway:

Aramark ranks at the bottom for Revenue Growth among its peers. It is in the middle for Gross Profit. Aramark is at the bottom for Return on Equity.

Delving into Aramark's Background

Aramark, founded in 1936 and headquartered in Philadelphia, Pennsylvania, operates as a food service company providing facility management and workplace solutions. The company primarily generates revenue from its North American food and support services segment, serving various clients including schools, healthcare facilities, and entertainment venues.

Aramark: Financial Performance Dissected

Market Capitalization Analysis: Reflecting a smaller scale, the company's market capitalization is positioned below industry averages. This could be attributed to factors such as growth expectations or operational capacity.

Revenue Growth: Over the 3 months period, Aramark showcased positive performance, achieving a revenue growth rate of 5.72% as of 30 June, 2025. This reflects a substantial increase in the company's top-line earnings. As compared to its peers, the revenue growth lags behind its industry peers. The company achieved a growth rate lower than the average among peers in Consumer Discretionary sector.

Net Margin: Aramark's net margin lags behind industry averages, suggesting challenges in maintaining strong profitability. With a net margin of 1.55%, the company may face hurdles in effective cost management.

Return on Equity (ROE): Aramark's ROE is below industry standards, pointing towards difficulties in efficiently utilizing equity capital. With an ROE of 2.35%, the company may encounter challenges in delivering satisfactory returns for shareholders.

Return on Assets (ROA): Aramark's ROA falls below industry averages, indicating challenges in efficiently utilizing assets. With an ROA of 0.54%, the company may face hurdles in generating optimal returns from its assets.

Debt Management: Aramark's debt-to-equity ratio is below the industry average at 2.14, reflecting a lower dependency on debt financing and a more conservative financial approach.

To track all earnings releases for Aramark visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.