Ameren's Earnings: A Preview

Ameren (NYSE:AEE) is gearing up to announce its quarterly earnings on Wednesday, 2025-11-05. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Ameren will report an earnings per share (EPS) of $2.11.

Anticipation surrounds Ameren's announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

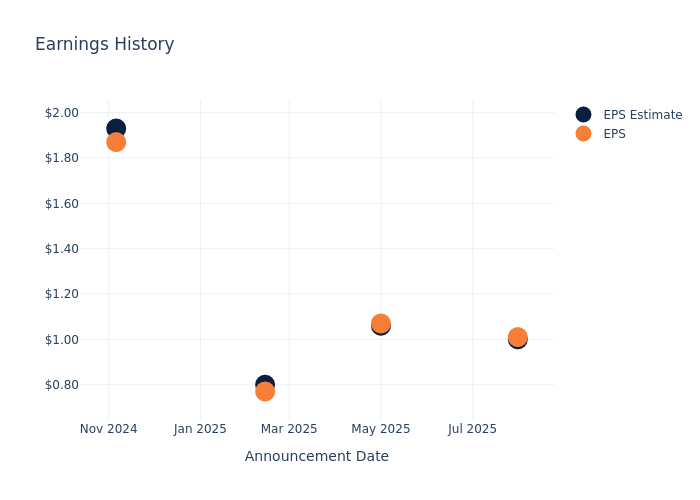

Earnings History Snapshot

The company's EPS beat by $0.01 in the last quarter, leading to a 0.97% increase in the share price on the following day.

Here's a look at Ameren's past performance and the resulting price change:

| Quarter | Q2 2025 | Q1 2025 | Q4 2024 | Q3 2024 |

|---|---|---|---|---|

| EPS Estimate | 1.00 | 1.06 | 0.80 | 1.93 |

| EPS Actual | 1.01 | 1.07 | 0.77 | 1.87 |

| Price Change % | 1.00 | 1.00 | 0.00 | -1.00 |

Ameren Share Price Analysis

Shares of Ameren were trading at $101.54 as of November 03. Over the last 52-week period, shares are up 15.76%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analyst Insights on Ameren

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding Ameren.

Ameren has received a total of 7 ratings from analysts, with the consensus rating as Neutral. With an average one-year price target of $111.43, the consensus suggests a potential 9.74% upside.

Comparing Ratings with Competitors

In this analysis, we delve into the analyst ratings and average 1-year price targets of DTE Energy, CenterPoint Energy and CMS Energy, three key industry players, offering insights into their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for DTE Energy, with an average 1-year price target of $147.75, suggesting a potential 45.51% upside.

- Analysts currently favor an Neutral trajectory for CenterPoint Energy, with an average 1-year price target of $41.5, suggesting a potential 59.13% downside.

- Analysts currently favor an Neutral trajectory for CMS Energy, with an average 1-year price target of $77.0, suggesting a potential 24.17% downside.

Insights: Peer Analysis

In the peer analysis summary, key metrics for DTE Energy, CenterPoint Energy and CMS Energy are highlighted, providing an understanding of their respective standings within the industry and offering insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Ameren | Neutral | 31.19% | $928M | 2.24% |

| DTE Energy | Neutral | 21.37% | $1.27B | 3.50% |

| CenterPoint Energy | Neutral | 7.11% | $1.03B | 2.66% |

| CMS Energy | Neutral | 15.95% | $876M | 3.27% |

Key Takeaway:

Ameren ranks in the middle for revenue growth among its peers. It has the lowest gross profit compared to others. Ameren's return on equity is also lower than some of its peers. Overall, Ameren's performance is average when compared to its peers in the industry.

All You Need to Know About Ameren

Ameren owns rate-regulated generation, transmission, and distribution networks that deliver electricity and natural gas through the company's two main subsidiaries, Ameren Missouri and Ameren Illinois. It serves 2.5 million electricity customers and approximately 1 million natural gas customers accross its two service territories.

Ameren: Delving into Financials

Market Capitalization: Boasting an elevated market capitalization, the company surpasses industry averages. This signals substantial size and strong market recognition.

Revenue Growth: Ameren's revenue growth over a period of 3 months has been noteworthy. As of 30 June, 2025, the company achieved a revenue growth rate of approximately 31.19%. This indicates a substantial increase in the company's top-line earnings. As compared to its peers, the company achieved a growth rate higher than the average among peers in Utilities sector.

Net Margin: Ameren's net margin surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive 12.38% net margin, the company effectively manages costs and achieves strong profitability.

Return on Equity (ROE): Ameren's financial strength is reflected in its exceptional ROE, which exceeds industry averages. With a remarkable ROE of 2.24%, the company showcases efficient use of equity capital and strong financial health.

Return on Assets (ROA): Ameren's financial strength is reflected in its exceptional ROA, which exceeds industry averages. With a remarkable ROA of 0.6%, the company showcases efficient use of assets and strong financial health.

Debt Management: The company maintains a balanced debt approach with a debt-to-equity ratio below industry norms, standing at 1.62.

To track all earnings releases for Ameren visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.